Life Lines:

Credit, Loans, and Debt

|

Up to this point, we've discussed the science of spending and saving, investing and planning. We even discussed risk management...but that was at the "national level". So...what about your own risk management? Seen through the concepts of credit cards, loans, and the debts associated with them? If I can keep you out of debt, I'd be a miracle worker. But! If I can keep you out of massive debt, then I'm a good teacher! Let's get started. |

|

Part I: Credit Cards and Debit Cards

Credit cards are everywhere. According to the site, NerdWallet.com, in 2009, 156 million Americans had a credit card, representing about half of the country’s population. And if this data’s from 2009, one can only assume what the statistics are today! Germans and Britons use credit cards frequently, but other European countries, such as France, Italy, and the Netherlands, use credit cards at far lesser rates, with French credit agencies issuing 4% fewer credit cards in 2013 compared with the previous year. Overall, however, the average European only retained 1.51 credit cards in 2013. By comparison, according to The Nilsson Report, the average American has 9.5 credit cards!!

Are credit cards good? Sure! Can they be bad? Of course! It’s all about how you use them.

So, what’s the best card for you, as an 18 year old? a 30 year old? a 50 year old? Let’s take a look.

Using the website, NerdWallet.com, we’ll be evaluating the best credit card options for 2015. Remember everything you’ve learned about interest rates and "risk vs. reward", and using the new-found knowledge of payment schedules, fine print, and hidden fees, Which card is the right one for you? Using your provided activity sheet and this website, let's get started!

Are credit cards good? Sure! Can they be bad? Of course! It’s all about how you use them.

So, what’s the best card for you, as an 18 year old? a 30 year old? a 50 year old? Let’s take a look.

Using the website, NerdWallet.com, we’ll be evaluating the best credit card options for 2015. Remember everything you’ve learned about interest rates and "risk vs. reward", and using the new-found knowledge of payment schedules, fine print, and hidden fees, Which card is the right one for you? Using your provided activity sheet and this website, let's get started!

Part II: Loans, Loans, Loans

Credit cards are just "plastic loans"; everytime you swipe your credit card, you're taking a loan out from a bank, asking for the bank to pay for that purchase, and you promise to pay them back in a short amount of time.

So...since you already understand credit cards, let's expand that concept a bit to loans in general. Throughout your life, you'll probably apply for the following loans:

So...since you already understand credit cards, let's expand that concept a bit to loans in general. Throughout your life, you'll probably apply for the following loans:

- A car loan (to buy a new or used car from a dealer or even a loan from a bank in order to have the money to purchase the car from a private seller)

- A home loan (known as a "mortgage"; a loan from a bank or credit agency in order to have money to buy a house)

- A college loan (to pay for college tuition, fees, and expenses)

There are other types of loans (payday loans, home equity loans, loans for business start up's, etc.), but these are the most common. Remember, a loan is not free money, and therefore, since the banks and lending agencies need to make money, they'll charge interest rates, that, on average, fall in the following ranges:

- A car loan ranges, typically from 3 - 5%, depending on a person's credit history, down payment, income, and other factors.

- A home loan ranges, typically from 3 - 6%, depending on a person's credit history, down payment, income, and other factors. In your parent's day, however, that rate could have been 10% or higher!

- A college loan ranges, typically from 2 - 10%, depending on a person's credit history, down payment, income, and other factors. It also depends on whether the loan is public or private, and (...frustratingly...) how much is left on that loan. Since these loans can be "variable", they may increase as you have less to pay! I know. Jerks! >:-/

|

Car loans and home loans don't seem to surprise people too much. If you have a "fixed rate", your interest rate is "carried" (like the percentage in red to the right...) at the same rate over the life of the loan. If your loan is "variable", your interest rate can "float (like the balloon in green...) throughout the life of the loan. For variable rates, the rate changes as national interest rates change as well...

|

|

As mentioned, car loans and home loans are not too surprising after your interest rate and repayment schedule. Car loans are usually repaid within five (5) years, but can be extended up to 7 years. Home loans ("mortgages") are usually paid over thirty (30) years. You'll usually make monthly payment, although sometimes it may be bi-monthly or even quarterly...

So let's go to college loans. Ugh. First of all, there's so much terminology! So, let's just start with a little quiz. Just do your best:

1) True or false: A federal loan is the same as a federal grant.

a) True

b) False

2) True or false: You do NOT have to know what college you want to attend in order to apply for scholarships.

a) True

b) False

3) According to the National Post-Secondary Student Aid Study, what percentage of 4-year undergraduates take out student loans?

a) 45%

b) 55%

c) 65%

d) 75%

4) How much can be deposited per child per year in an Education IRA?

a) $300

b) $400

c) $500

d) $600

Not easy, huh? Answers?

So, before we start the hard-core stuff, let's start with some basic facts!

So let's go to college loans. Ugh. First of all, there's so much terminology! So, let's just start with a little quiz. Just do your best:

1) True or false: A federal loan is the same as a federal grant.

a) True

b) False

2) True or false: You do NOT have to know what college you want to attend in order to apply for scholarships.

a) True

b) False

3) According to the National Post-Secondary Student Aid Study, what percentage of 4-year undergraduates take out student loans?

a) 45%

b) 55%

c) 65%

d) 75%

4) How much can be deposited per child per year in an Education IRA?

a) $300

b) $400

c) $500

d) $600

Not easy, huh? Answers?

- FALSE. Federal grants and loans are NOT the same;

- TRUE. You do NOT have to know what school you're going to in order to apply for scholarships.

- 65% of students take out loans!

- $500 per child, per year, can deposited in an Educational IRA.

So, before we start the hard-core stuff, let's start with some basic facts!

Fact #1: There is a difference between

a Grant, a Scholarship, and a Loan.

A grant is an award given, usually by a school or institution, for the purposes of school. Think of it as "gift" money, but it's often given for educational costs only. A scholarship is similar, but can be given by private businesses and individuals, and may or may not be "renewable": It might just be $1,000 total, and NOT $1,000 per year over the course of your college career. Additionally, a scholarship can often be used for living expenses and not just school-related costs. A loan is NOT a gift, and must be paid back, with interest.

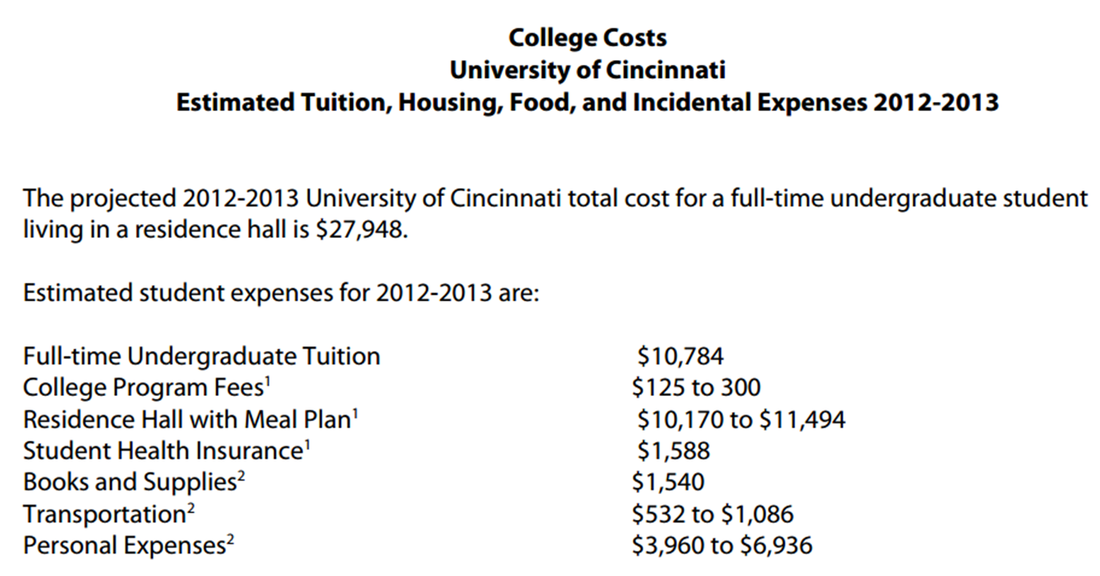

Fact #2: "College Costs"

are not just for "Classes"

In fact, the most expensive part of your freshman year is living on campus! See a screenshot of the costs of attending the University of Cincinnati below:

Fact #3: College Costs Vary by Year

For many, Freshman year is the most expensive as you're most likely living on campus. It's often cheaper to live off campus, and therefore, the costs are lower. Additionally, books are more expensive Freshman year for a few reasons: 1) Introductory Freshman courses are more "textbook" based, rather than traditional book based, and therefore more expensive. 2) Freshman tend to buy all the books suggested by the professor instead of waiting to see if the books are actually required. Just wait to see if you'll actually need them!

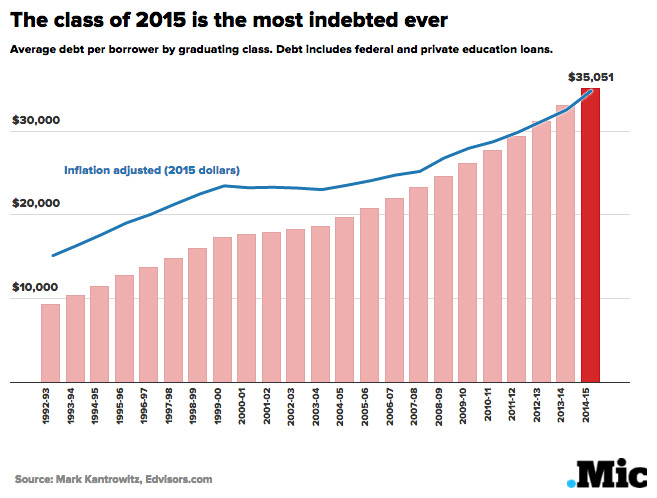

Fact #4: College is Still a Good Investment

...For Now

College is very expensive, but in today's economy, a bachelor's degree is required by most jobs. However, the Class of 2015 is the most indebted class ever. Only time will tell if college will remain the best investment. But for now, and for the next few years...it still is.

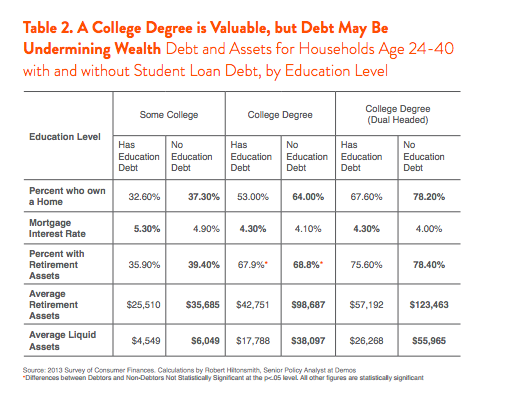

...and this debt is preventing those college graduates from 1) Owning a home, 2) Saving for Retirement, and 3) Accessing liquid assets:

Fact #5: All Loans are NOT Created Equal

And that's where we'll spend most our time today. This website offers a "Start to Finish" overview of the loan process.

What Do I Want You To Do?

|

I want you to be an educated consumer! I want you to attack this college loan process! No offense to those loan people, but they make money on you NOT KNOWING your options! Don't be stupid! Be informed! Be offensive, not defensive. Be proactive, not reactive. I don't want you to be like Uncle Sam on the right...victim to the loan process and college debt in general! But more specifically, I want you to tool around on those two websites, playing a "scavenger hunt" of sorts, defining key vocabulary, necessary steps, the "chronology of process", etc. etc. Use your provided activity sheet for the "scavenger hunt". |

|

|

And if you get done, have fun on this site! It's kinda like an eHarmony "college search" that "matches" you, and your desires, to colleges across the country! Yes, I know most of you will stay "in state", but why? Do you want to? Or do you just not know of other options? This is a really cool site. So, have fun! And this summer (or fall...), check out some of these sites!

|